by Wise Financial Group, Inc. | Nov 18, 2020 | Tax Tips and News

Fiscal Year 2020 was a very busy—and productive—year for the IRS’ Criminal Investigations unit. The just-released annual report for CI Division touts the unit’s identification of more than $10 billion in tax fraud and other financial crimes, despite the limitations of the COVID-19 pandemic.

This made IRS Commissioner Chuck Rettig a very happy man.

“The special agents and professional staff who make up Criminal Investigation continue to perform at an incredibly high-level year after year,” said Commissioner Rettig. “Even in the face of a global pandemic, the CI workforce initiated nearly 1,600 investigations and identified $2.3 billion in tax fraud schemes. This is no small feat during a challenging year, and their work is critical to protecting taxpayers and the integrity of our tax system.”

IRS investigators had plenty of work to keep them busy in 2020, examining COVID-19-related fraud, cybercrimes, virtual and cryptocurrencies, traditional tax investigations, international tax enforcement, employment tax, refund fraud and tax-related identity theft.

The IRS is changing tactics to keep up with perpetrators.

In response to COVID-19-related cases, CI special agents adapted their investigative techniques to initiate cases into fraudulent claims for Economic Impact Payments, Paycheck Protection Program loans, and refundable payroll tax credits from the Coronavirus Aid, Relief, and Economic Security Act (also known as the CARES Act).

“This year, more than any in recent memory, demonstrated the extraordinary agility and adaptability of the CI workforce,” said Jim Lee, Chief of CI. “Clearly, unscrupulous individuals sought to exploit the economic safeguards put in place to buttress a nation in crisis. These individuals and groups were instead met with a cadre of special agents determined to thwart their efforts.”

It should be noted that Lee took over the reins of CI just this year, after the retiring Don Fort, named Lee the new chief, capping his long career in the division.

In fiscal year 2020, CI initiated 1,598 cases, devoting 73% of its time to tax-related investigations. The number of CI special agents increased by just one percent; new special agents were hired to offset planned retirements.

CI increased and improved its data analyses while strengthening its international partnerships to assist in finding the most impactful cases.

One important partnership remained the Joint Chiefs of Global Tax Enforcement (J5), a trans-national committee comprised of tax organizations from five countries. In FY 2020 alone, more information was shared on cryptocurrency, tax crimes and related enforcement, than in the previous 10 years combined. CI also saw the first guilty pleas for a case brought to justice under the J5 umbrella.

CI is the only federal law enforcement agency with jurisdiction over federal tax crimes. As such, the division has one of the highest conviction rates in federal law enforcement: 90.4%.

IRS leadership says the high conviction rate is a testament to the department’s thoroughness of CI investigations and the quality of its special agents. CI is routinely called upon by prosecutors and partner agencies across the U.S. to lead financial investigations on a wide variety of financial crimes.

“While the annual report is an excellent summation of the hard work and dedication exhibited by CI, this year’s report takes on special significance,” Lee said. “This report unequivocally reflects the efforts of a workforce undaunted by unprecedented personal and professional challenges. I am profoundly grateful to serve with the men and women of CI.”

The interactive 2020 report summarizes a variety of CI activities during the fiscal year and highlights examples of cases for each field office on a wide range of financial crimes. The fiscal year begins Oct. 1 and ends on Sept. 30.

– Story provided by TaxingSubjects.com

by Wise Financial Group, Inc. | Nov 18, 2020 | Tax Tips and News

With 2020’s extended tax deadlines due to the coronavirus pandemic, it seems like we just wrapped up the previous tax season. But believe it or not, the next filing season kicks off Jan. 1, 2021.

The Internal Revenue Service is encouraging taxpayers to begin organizing their tax-related documents now, to avoid confusion later on. The IRS has even put together a special web page that outlines the steps that taxpayers can take now to prepare for the 2021 filing season.

Make filing easier in ‘21.

The first step toward filing, of course is to gather the necessary paperwork or electronic files that every taxpayer needs to file. Forms W-2, Wage and Tax Statement; Forms 1099-MISC, Miscellaneous Income; and other income documents help determine if the taxpayer is eligible for deductions or credits.

They’ll also need their Notice 1444, Economic Impact Payment, to calculate any Recovery Rebate Credit they may be eligible for on their 2020 federal income tax return.

The best rule of thumb is that most income is taxable, including unemployment compensation, refund interest and income from the gig economy and virtual currencies.

Taxpayers with an Individual Taxpayer Identification Number (ITIN) should ensure it hasn’t expired before they file their 2020 tax return. If it has expired, the IRS recommends they submit a Form W-7, Application for IRS Individual Identification Number, now to renew their ITIN.

Taxpayers who fail to renew an ITIN before filing a tax return next year could face a delayed refund and could even be ineligible for certain tax credits.

Also on the income side, taxpayers can use the Tax Withholding Estimator on IRS.gov to help calculate the right amount of tax to have withheld from their paychecks. If they need to adjust withholding for the remainder of the year, time is running out. It’s best to submit a new Form W-4, Employee’s Withholding Certificate, to their employer as soon as possible.

Those who received non-wage income like self-employment income, investment income, taxable Social Security benefits, and in some instances, pension and annuity income, may have to make estimated tax payments.

Payment options can be found at IRS.gov/payments.

No EIP? Check into the Recovery Rebate Credit!

Taxpayers may be able to claim the Recovery Rebate Credit if they met the eligibility criteria in 2020 and:

- They didn’t receive an Economic Impact Payment this year, or

- Their Economic Impact Payment was less than $1,200 ($2,400 if married filing jointly for 2019 or 2018) plus $500 for each qualifying child.

- For additional information about the Economic Impact Payment, taxpayers can visit the Economic Impact Payment Information Center.

Interest on a refund is taxable.

Taxpayers who got a federal tax refund in 2020 may have been paid interest. The IRS sent interest payments to individual taxpayers who timely filed their 2019 federal income tax returns and received refunds. Most interest payments were received separately from tax refunds.

Interest payments are taxable and must be reported on 2020 federal income tax returns. In January 2021, the IRS will send a Form 1099-INT, Interest Income, to anyone who received interest totaling at least $10.

Although the IRS issues most refunds in less than 21 days, the IRS cautions taxpayers not to rely on receiving a 2020 federal tax refund by a certain date, especially when making major purchases or paying bills. Some returns may require additional review and may take longer.

Some Refunds Not Available Until March

By law, the IRS can’t issue refunds for people claiming the Earned Income Tax Credit (EITC) or Additional Child Tax Credit (ACTC) before the middle of February. The law requires the IRS to hold the entire refund – even the portion not associated with either the EITC or ACTC.

The IRS expects most refunds related to these two credits to be available in taxpayer bank accounts or on debit cards by the first week of March if they chose direct deposit and there aren’t any other issues with their tax return.

Taxpayers should use the Where’s My Refund? online tool to track their refund payment.

Stay home and stay safe with IRS online tools.

Taxpayers can find online tools and resources to help get the information they need. These IRS.gov tools are easy-to-use and available 24 hours a day. Millions of people use them to find information about their accounts, get answers to tax questions or file and pay their taxes.

Taxpayers also have several options to find a tax preparer. One resource is Choosing a Tax Professional, which offers a wealth of information for selecting a tax professional.

The Directory of Federal Tax Return Preparers with Credentials and Select Qualifications can help taxpayers find preparers in their area who currently hold professional credentials recognized by the IRS, or who hold an Annual Filing Season Program Record of Completion.

Source: IR-2020-256

– Story provided by TaxingSubjects.com

by Wise Financial Group, Inc. | Nov 16, 2020 | Tax Tips and News

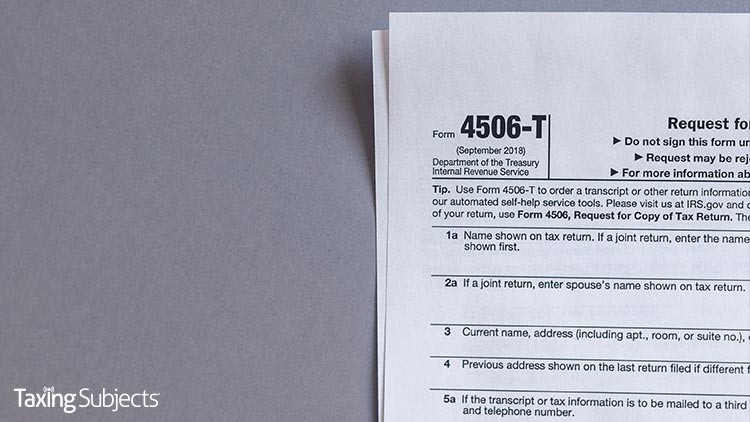

After Dec. 12, business tax transcripts will soon be a little less informative—for good reason. The IRS will start masking sensitive data on the transcripts to protect businesses from identity theft beginning Dec. 13.

The announcement from the IRS provides 30 days for adjustments from stakeholders. The agency started informing tax pros of the change during the Nationwide Tax Forums during the summer.

The IRS started masking similar data on individual tax transcripts two years ago.

A tax transcript is a summary of a tax return. They are often used by tax practitioners to prepare prior-year tax returns or to represent the client before the IRS. Lenders and others use tax transcripts for income verification purposes.

What’s visible on the new transcript?

After Dec. 12, here’s what you can expect to see on the reworked transcripts:

- Last four digits of any Employer Identification Number listed on the transcript: XX-XXX1234

- Last four digits of any Social Security number or Individual Tax Identification Number listed on the transcript: XXX-XX-1234

- Last four digits of any account or telephone number

- First four characters of the first, and last name for any individual (first three characters if the name has only four letters)

- First four characters of any name on the business name line

- First six characters of the street address, including spaces

- All money amounts, including wage and income, balance due, interest and penalties

For both the individual and business tax transcript, there is space for a Customer File Number. The Customer File Number is an optional 10-digit number that can be created usually by third parties that allow them to match a transcript to a taxpayer.

The Customer File Number field will appear on the transcript when that number is entered on Line 5 of Form 4506-T, Request for Transcript of Tax Return, and Form 4506T-EZ.

How do you verify income for a lender?

Here’s how the new transcript design will work for a taxpayer seeking to verify income for a lender:

- The lender assigns a 10-digit number (such as a loan number, for example) to the Form 4506-T. The Form 4506-T may be signed and submitted by the taxpayer, or signed by the taxpayer and submitted by the lender.

- The Customer File Number assigned by the requestor on the Form 4506-T will populate on the transcript. The requestor can assign any number except the taxpayer’s Social Security Number or Employer Identification Number.

- Once the requestor gets the transcript, its Customer File Number serves as a tracking number to link the document to the taxpayer.

For more information about masking transcripts, consult the IRS e-Services web page after Dec. 13.

Source: IR-2020-254

– Story provided by TaxingSubjects.com

by Wise Financial Group, Inc. | Nov 13, 2020 | Tax Tips and News

Some people managed to register for their $1,200 Economic Impact Payment (EIP) but just didn’t have the necessary information in-hand to also sign up for the $500 payment for qualifying children.

Now the IRS says there’s a way to get that missing payment. The Internal Revenue Service has announced that federal beneficiaries who didn’t register—or weren’t able to register—to get the $500-per-child payments earlier this year now have more time to do so.

The agency has made programming changes to its computers, allowing anyone who registers using the Non-Filers: Enter Info Here tool before the 3 p.m. Eastern Time Nov. 21 extended due date will receive an EIP, if they’re eligible.

The extension covers includes federal beneficiaries who already received their EIP but did not get an additional $500 payment for qualifying children. It allows them to enter the necessary information on their qualifying children using the Non-Filers tool on the IRS website.

Who qualifies?

Those who are eligible to input the information include people with qualifying children who get Social Security retirement, survivor or disability benefits, Supplemental Security Income (SSI), Railroad Retirement benefits or Veterans Affairs Compensation and Pension (C&P) and did not file a tax return in either 2018 or 2019.

In addition, anyone who didn’t have a requirement to file a tax return in 2018 or 2019 is being urged by the agency to register for an Economic Impact Payment using the Non-Filers tool on IRS.gov before the Nov. 21 deadline.

Once registered, applicants can speed up their payment by opting to get it by direct deposit. Those not choosing direct deposit will get a paper check through the mail. Once registered, recipients can track the status of their payment using the Get My Payment tool, available only on IRS.gov.

– Story provided by TaxingSubjects.com

by Wise Financial Group, Inc. | Nov 12, 2020 | Tax Tips and News

A new notice from the Internal Revenue Service reveals some new rules that are expected to be included in upcoming proposed regulations.

Notice 2020-75 spells out the proposed regulations clarifying that state and local income taxes imposed on and paid by a partnership or S corporation on its income are allowed to be claimed as a deduction by the filing partnership or S corp.

The filing entity, the notice continues, would use the state and local taxes paid to calculate its non-separately stated taxable income or loss for the taxable year of payment. Therefore, the notice concludes, the tax payments are not subject to the limitation for state and local taxes on partners and shareholders who itemize deductions.

“This definition does not include income taxes imposed by U.S. territories or their political subdivisions,” the notice states. “Thus, this definition solely includes income taxes described in section 164(b)(2) for which a deduction by a partnership is not disallowed under section 703(a)(2)(B), and such income taxes for which a deduction by an S corporation is not disallowed under section 1363(b)(2).”

Further, the notice puts the changes in play immediately and details when the new rules can be applied to specified tax payments:

“The proposed regulations described in this notice will apply to Specified Income Tax Payments made on or after November 9, 2020.The proposed regulations will also permit taxpayers described in section 3.02 of this notice to apply the rules described in this notice to Specified Income Tax Payments made in a taxable year of the partnership or S corporation ending after December 31, 2017, and made before November 9, 2020, provided that the Specified Income Tax Payment is made to satisfy the liability for income tax imposed on the partnership or S corporation pursuant to a law enacted prior to November 9, 2020.”

For updates on the implementation of the Tax Cuts and Jobs Act (TCJA), check out the Tax Reform page on IRS.gov.

Source: IR-2020-252

– Story provided by TaxingSubjects.com

Wise Financial Group, Inc.

Wise Financial Group, Inc.